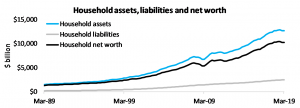

Quarterly data from the ABS showed that at the end of the March 2019 quarter, household net worth was $10.243 trillion. While that is certainly a large figure, household wealth has now fallen for two consecutive quarters and is -0.7% lower year-on-year. The $10.243 trillion in net worth is made-up of $12.701 trillion in assets and $2.458 trillion in liabilities. The recent fall in the value of assets at a time in which liabilities have continued to rise has led to the fall in net worth.

The Reserve Bank (RBA) takes this data and produces a number of valuable ratios, including: debt, assets and interest payments to household disposable income. These ratios highlight the impact of high levels of debt at a time in which asset values have fallen but the debt has not fallen at the same pace.

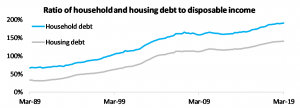

The ratio of household debt to disposable income has continued to climb over the quarter, reaching a new historic high of 189.7%. The rise in household debt relative to incomes has certainly slowed but it continues to edge higher. The ratio of housing debt to disposable income is recorded at 140.1% and was unchanged over the quarter. While it was unchanged over the quarter it remains at an historic high level, highlighting that households remain very sensitive to the cost of mortgage debt.

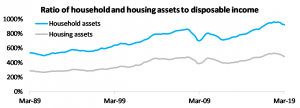

Turning to the ratio of household assets to disposable income, it was recorded at 927.0% in March 2019. The ratio peaked at 961.7% in December 2017 and has trended lower since. The ratio of housing assets to disposable income peaked at 529.6% in December 2017 and as at March 2019 it was recorded at 483.5%. The reduction in housing values has coincided with the period in which the ratio of household and housing assets has fallen which is no wonder when you consider housing accounts for around half of the value of household assets. Also important to consider is that while the value of assets are falling there has been no reduction in the ratios of debt to income highlighting that asset depreciation has been greater than debt reduction. As a result, the ratio of household debts to assets is at 20.5%, the highest it has been since December 2014 and the ratio of housing debt to assets is at 29.0%, the highest it has been since June 2013.

Despite the lowest interest rates since the 1960s, the ratio of interest payments to disposable income has trended higheryears. As at March 2019 the ratio was recorded at 9.1% and although it has been steady for three quarters, interest payments relative to disposable income has trended higher on an annual basis. Furthermore, the ratio of interest payments to disposable income was last this high in September 2013. It’s a similar story for the ratio of housing interest payments to disposable income which is also trending higher, recorded at 7.6%, which is the highest ratio since June 2013.

With interest rates at generational lows there was perhaps, some expectation that households would use the low rates to pay off some debt however, that has largely not occurred. With asset values recently falling the data shows that debt pay off has not been as rapid as the declines leading to a reduction in household wealth.

This data is to March 2019 and by the end of June 2019 there were some tentative signs that the declines in dwelling values were starting to level. While this means that there is likely to be a further decline in household wealth over the June quarter, it also suggests there is unlikely to be a meaningful reduction in household debt levels. As such household debt levels are likely to remain amongst the highest in the world. At the same time, the value of household assets remain substantially higher than the value of the debt. The cause for concern will be what happens if economic conditions deteriorate materially, leading to weaker labour market conditions and potentially creating some challenges around servicing such high levels of debt as unemployment rises.

Another medium to long term consideration is a scenario where interest rates eventually start to rise. Households are generally able to service high levels of household debt while interest rates are at record lows, but eventually (probably not for at least several years) interest rates will rise. If household debt levels remain high relative to incomes under a higher interest rate environment, the result could be weakness in household spending (as households dedicate more of their income towards servicing their debt) and potentially higher levels of financial stress amongst heavily leveraged households.

Source: RP Data Core Logic